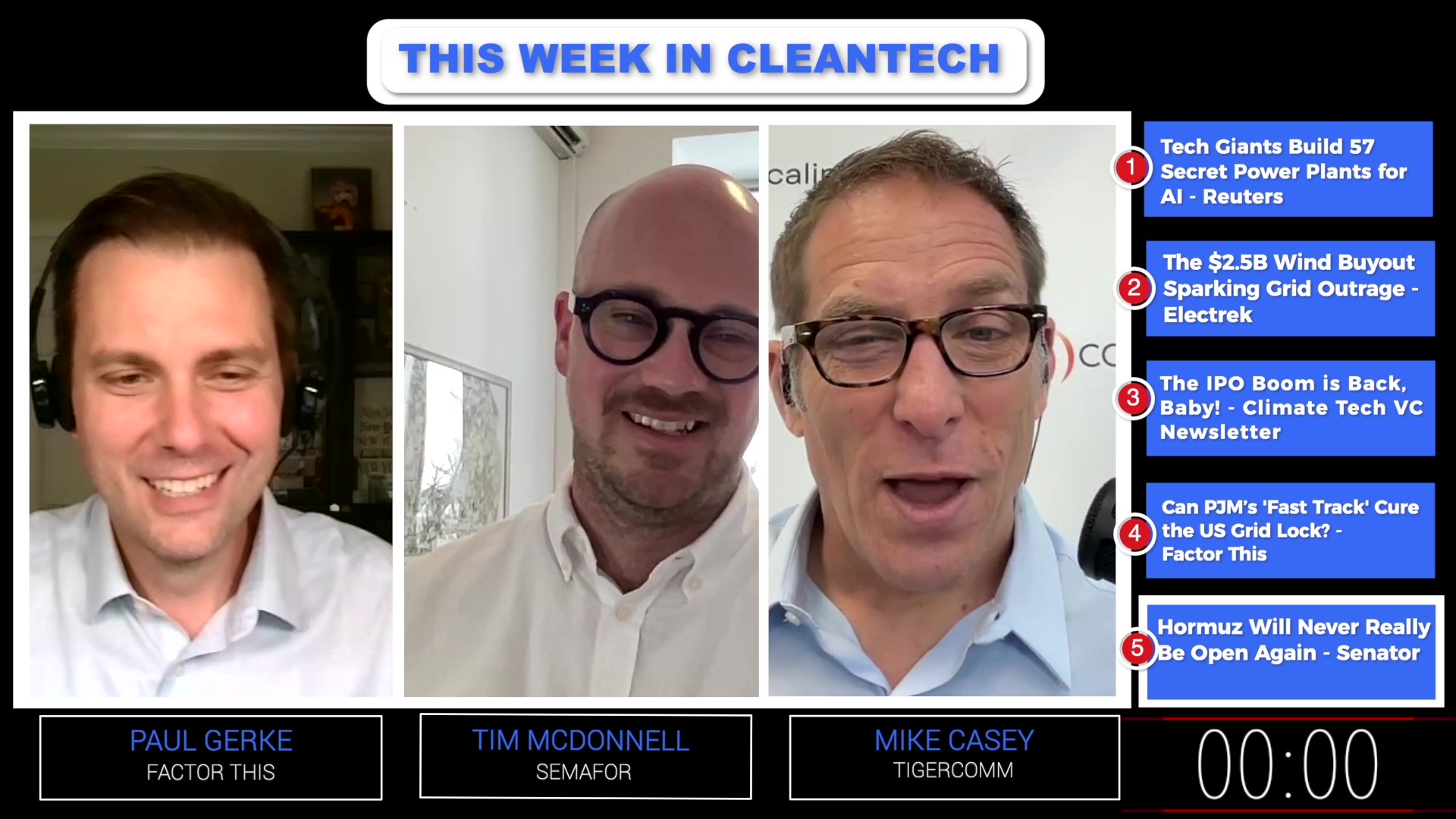

This Week in Cleantech is a weekly podcast covering the most impactful stories in clean energy and climate featuring Paul Gerke of Factor This and Tigercomm’s Mike Casey.

This week’s episode features special guest Tim McDonnell from Semafor, who discusses the potential future of the Strait of Hormuz and energy markets if the US-Iran de-escalation deal holds.

This week’s “Cleantecher of the Week” is Andrew Redd, CEO of Endurance Energy, a Seattle-based seafloor geothermal energy developer, which just raised $54m in Series A funding. Redd is a former SpaceX engineer who is now drilling into spots at the bottom of the ocean where tectonic plates split apart and magma heats the water to over 700 degrees. Congratulations Andrew!

Meta’s 800-acre Bowling Green data center in Ohio is one of dozens of large, off-grid power projects being approved in just weeks or months, without the years of permitting, environmental studies, or public hearings typically required for plants like this. Developers argue these off-grid plants serving private customers are exempt from many of those rules.

To keep things quiet, some developers have used NDAs with local governments or operated through shell companies, while local officials have redacted public documents or fast-tracked permits that would’ve otherwise triggered public hearings.

The Interior Department cut another near-billion-dollar deal to walk away from offshore wind and pivot to gas. This time, $765 million to Invenergy to cancel four leases off New York, New Jersey, California, and Maine, in exchange for redirecting that capital into domestic gas projects.

That brings the total to roughly $2.6 billion across three deals this year, all aimed at shifting companies off cheap, clean wind and onto dirtier, more expensive gas. And these payouts come from the Judgment Fund, which exists to settle lawsuits against the government, but no lawsuit was ever filed.

Back in 2020 and 2021, a wave of climate and EV startups went public through SPACs — blank-check shells that let you skip normal IPO scrutiny. A lot of companies had little revenue, missed badly, and collapsed.

Three years after that bust, climate tech is back. Listings are up 83% off their 2024 trough. But this time it’s a real IPO story, not just SPACs, and energy is the leading vertical, where transportation led last time. The headliners are nuclear and geothermal.

There is a quieter group of energy services and equipment companies like Legence, SOLV Energy, and ERock — as arguably more commercially grounded, with $1 to $3 billion in trailing revenue that can deploy today.

FERC approved PJM’s new Expedited Interconnection Track on June 9, a temporary fast-track pathway to bring large, shovel-ready generation projects online faster. PJM needs roughly 15,000 MW of new capacity to cover its deficiency, largely driven by the data center load swarming its system.

The track allows up to 10 projects per year, each over 250 MW, any fuel type including storage. Projects have to be sponsored by a PJM state, interconnect within that state, prove 100% site control, and reach commercial operation within three years. PJM expects to turn around an interconnection agreement in about 10 months versus the usual slog.

The US-Iran deal may restore tanker traffic and lower oil prices (Goldman cut its Q4 Brent forecast from $90 to $80), though clearing tankers and rebuilding could take months. Despite over a billion barrels lost since February, prices never topped the 2022 Ukraine spike, thanks to US “energy dominance,” strategic reserves, and clean energy.

Long-term, electrification is accelerating and geopolitics is shifting from tankers toward minerals, grids, and batteries, while the Strait of Hormuz loses importance as Gulf states build bypasses and compete. The US no longer reliably guarantees global energy security, and its dominance helped American consumers at allies’ expense.

Want to make a suggestion for This Week in Cleantech? Nominate the stories that caught your eye each week by emailing [email protected]